Projects in Dubai Healthcare City 2

AED 1.5M

AED 829K

AED 1.9M

AED 1.9M

AED 2.9M

AED 2M

Nearby Projects

Other Developers

Explore by Developer in Dubai Healthcare City 2

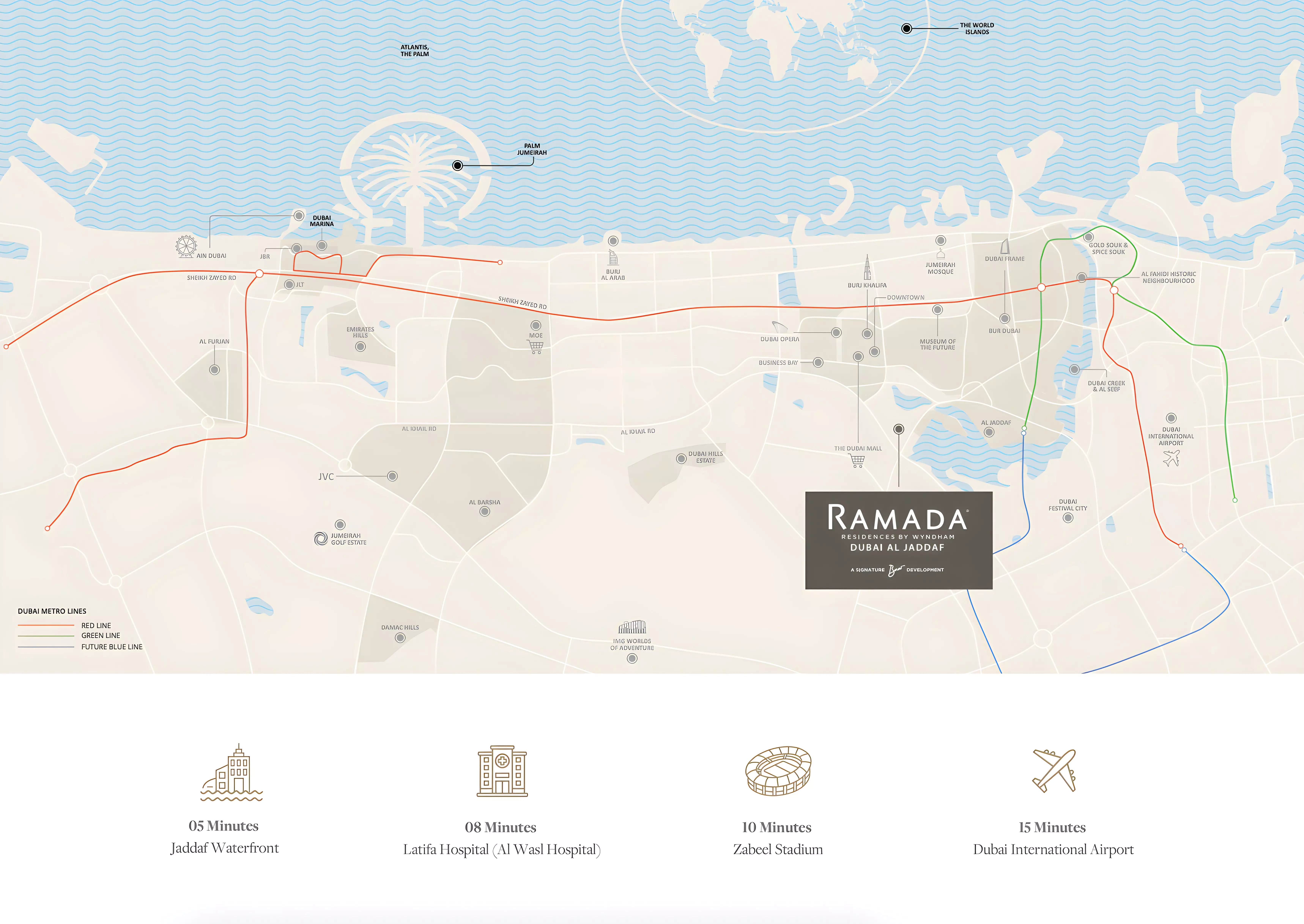

Where Al Jaddaf Meets the Creek: New Projects in Dubai Healthcare City 2

Dubai Healthcare City 2 sits within Al Jaddaf, directly adjacent to Dubai Creek and a short distance from Ras Al Khor. The subdistrict takes its name from the broader healthcare zone but has developed into a mixed residential corridor with a defined, if compact, set of options. Active projects here include Azizi David, Binghatti Ivory, Binghatti Starlight, Creek Views 3, Kempinski Residences The Creek, and Ramada Residences by Wyndham. Six projects across four developers means the market is legible but not deep. Buyers have a clear picture of what is available; the trade-off is limited room to compare and negotiate.

A Median at AED 1.87 Million

Pricing spans AED 829,000 at the entry level to AED 8,387,500 at the top, with a median of AED 1,875,246. That is a tenfold gap, which reflects the range of product types rather than instability in a single tier. Buyers entering near the median are looking at mid-sized apartments. The duplex and penthouse product push the ceiling considerably higher.

| Property Type | Projects |

|---|---|

| Apartment | 6 |

| Duplex | 2 |

| Penthouse | 1 |

Apartments are the dominant product, making this subdistrict more relevant to investors and single or small-household buyers than to families seeking larger internal volumes. Duplexes signal a step-up buyer who wants more space without leaving the zone. The single penthouse sits in a category of its own at the top of the range.

Four Developers and What That Means for Resale

Azizi Developments and Binghatti Developers are the most recognisable names here, alongside BNW Developments and Swiss Property. Azizi and Binghatti carry track records and brand presence that tend to support secondary market liquidity in Dubai. BNW and Swiss Property are smaller players with fewer completed projects publicly on record. With six projects spread across four developers, no single name controls the subdistrict. Buyers prioritising resale value should factor developer familiarity into their shortlisting decisions, as brand recognition plays a meaningful role in buyer demand when it comes time to sell.

Handover Timing and Entry Costs

The earliest completion on record is July 2025, which means at least one project has likely already handed over or is in its final stages. Buyers looking at those units should verify current construction and handover status directly before proceeding. The latest completion extends to December 2027, leaving roughly 18 months of off-plan window from mid-2026 for the newest launches. None of the projects here carry post-handover payment plans, so buyers should plan for full payment to be settled by handover. The minimum down payment across the market is 10%, which sits at the lower end of standard Dubai off-plan requirements.

What the Amenities Point To

The recurring amenities across these projects are gymnasium, health club, indoor swimming pool, CCTV security, security staffing, and landscaped gardens. A children's play area appears alongside restaurants and valet parking, the latter suggesting at least one project operates closer to a serviced residence model. Taken together, the amenity pattern favours structured building management and wellness infrastructure over destination lifestyle features. That matches Al Jaddaf's broader character as a functioning residential district with a professional resident base rather than a leisure-led development zone.